Transforming Inventory into Profit

Did you know that your Purchasing Department can add profit to your bottom line faster than your Sales Department?

For example, a typical industrial sales representative might take 2-4 weeks to generate $100,000 in sales, resulting in approximately $3,500 in net profit before taxes.

In comparison, the Purchasing Department can achieve the same result in just an afternoon.

Here’s how: by purchasing $10,000 worth of fast-moving stock from The DeadStock Broker at a cost of $6,500, you instantly save $3,500, which goes directly to your bottom line.

Inventory Metrics

Measuring the impact of reducing dead inventory and optimizing purchasing requires tracking specific key performance indicators (KPIs) and comparing them before and after implementing your strategies. Here’s a breakdown of how you can measure these impacts effectively:

Dead Inventory Reduction

Explanation: This formula calculates the percentage decrease in dead inventory over a period.

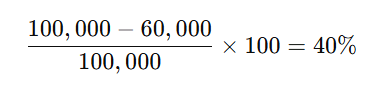

- Starting Dead Inventory Value: The total value of inventory classified as “dead” at the beginning of the measurement period.

- Ending Dead Inventory Value: The total value of dead inventory at the end of the measurement period.

Use Case: This is a performance metric to measure how effectively dead inventory has been reduced. For example, if you start with $100,000 in dead inventory and reduce it to $60,000, the reduction percentage is:

Inventory Turnover Ratio

- Measure: How efficiently inventory is being sold and replaced.

- Goal: A higher ratio indicates better inventory management.

- Explanation: This ratio measures how efficiently inventory is sold and replaced during a specific period.

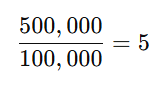

- Cost of Goods Sold (COGS): The direct costs of producing or purchasing the goods that have been sold.

- Average Inventory: The average value of inventory on hand during the period, typically calculated as

- Use Case: A higher turnover ratio indicates efficient inventory management. For instance, if COGS is $500,000 and average inventory is $100,000:

This means inventory turns over 5 times per year.

Financial Metrics

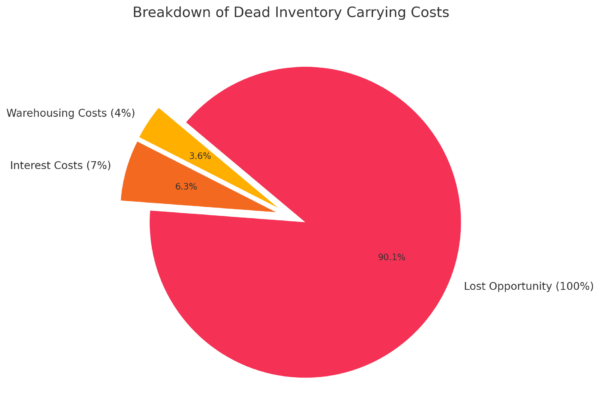

Cost Savings from Reduced Carrying Costs

- Measure: Reduction in carrying costs due to reduced dead inventory.

![]()

- Explanation: This formula estimates the financial impact of reducing dead or excess inventory.

- Reduction in Inventory Value: The decrease in inventory classified as dead or excess.

- Carrying Cost Percentage: The percentage cost of holding inventory, including warehousing, interest, and depreciation.

- Use Case: If you reduce $80,000 of dead inventory and the carrying cost is 30%, the savings are:

This $24,000 directly improves your profit.

Profit Margin Improvement

- Measure: Impact of cost savings and inventory optimization on profit margins.

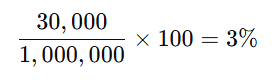

- Explanation: This metric evaluates how much profit a business retains from its total sales.

- Net Profit: The profit remaining after all expenses, taxes, and costs.

- Total Sales: The total revenue generated from sales.

- Use Case: If your net profit is $30,000 and total sales are $1,000,000:

This shows that 3% of your sales revenue is retained as profit.